Fintech Security & Compliance — Part 1

Fintech is one of the most happening sectors in India & world over with a wide array of services being delivered in lending, insurance, payments, stocks and mutual funds. While founders, product and engineering managers are busy in building the products and delivering them to the people in a rapid and scalable way, there is one huge challenge they must overcome. And that’s the Cyber Security aspect of it. I have had the opportunity to architect and implement controls around these requirements in the last few years and would like to share some thoughts here.

In India, Fintech regulators are:

- Securities & Exchange Board of India (SEBI)

- Reserve Bank of India (RBI)

- Insurance Regulatory and Development Authority of India (IRDAI)

Each of these regulators have their own cybersecurity requirements and these span across multiple domains of cybersecurity like IT Governance, Information Security Audits (IS Audits), IT Outsourcing, IT Risk Management, Business Continuity Management (Good luck on a single region currently offered by the leading cloud vendor in India 🙂 ), Policies, Physical & Environment Security and etc

Apart from these, compliance with PCI DSS/PA DSS is a common requirement for all the fintechs handling credit card transactions. When it comes to PCI DSS, the magnitude of security requirements vary based on the volume of transactions. There are Four Merchant levels starting with Level 4 wherein a merchant handles 20,000 plus transactions and compliance requires that you fill a Self Assessment Questionnaire to Level 1 where 6 million plus transactions are handled annually. Level 2 and 1 have very comprehensive requirements to fulfil and are audited by a third-party.

Not all the Fintechs have the license to operate independently and they leverage the agreements with Banks/Financial institutions to offer the services. It would be surprising to know that banks themselves can offer most of the services which fintechs are offering. The key underlying factor here is Technology, which perhaps banks are yet to come to terms with. When it comes to security requirements and compliances, banks pass on these to the partnering fintechs. So multiple audits in a year are not unheard of in the fintech space.

RBI has Master Directions for entities operating in the banking/non-banking space covering Lending, Loans, Prepaid Payment Instruments, Non-Banking Finance Company (NBFC), Peer to Peer Lending companies, Full fledged banks, Payments Banks and so on.

IRDA has two two major cyber security requirements and one of them is meant exclusively for insurance offered on e-com channels like web/mobile/app channels called ISNP — Insurance Self Networking Platform. As most of the new-age insurance companies are ecom based, they are forced to comply with both (there is some overhead here).

IRDA’s requirement has a cybersecurity checklist with 307 controls and also mandates a Chief Information Security Officer (CISO) to be appointed by the insurance company! While these may be easier to implement for a legacy company with the monolithic architecture, startups usually find these difficult and herein lies the challenge.

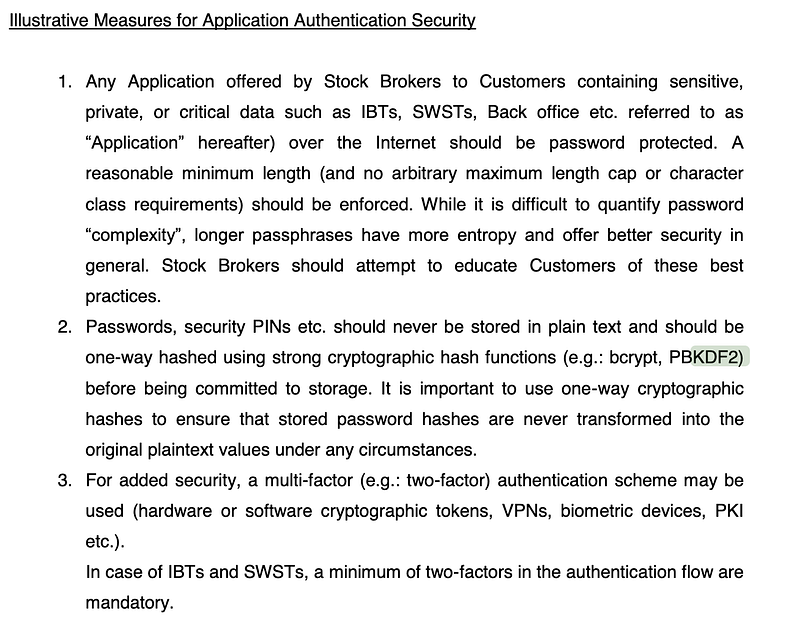

SEBI’s framework for Stock Brokers and Depository participants is published here — What I found cool about SEBI’s directives on Cyber Security in comparison to RBI and IRDA is its forward looking approach and in sync with current demands and realities. For example they suggest using Bcrypt / PDKDF2 for hashing passwords, usage of passphrases vs complex passwords:

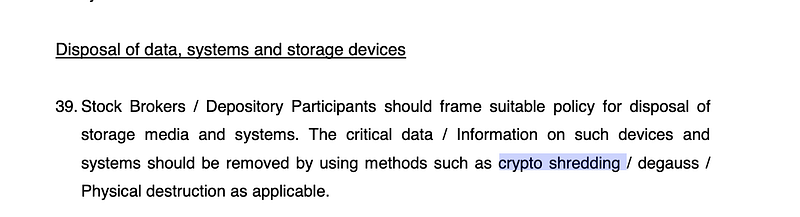

Also has a reference to Crypto Shredding, must confess I did not know such a terminology existed:

It makes me wonder if the major innovations in the fintech space in India is in the segment operated by the SEBI for reasons like these.

I am thinking of writing in detail about the challenges in complying with the security directives by the regulators in coming writeups but for now will focus on what this augurs for cybersecurity professionals in startups/fintechs.

There is going to be a huge demand for not just Developers, Product Managers, Architects, Data Scientists, but also Cyber Security professionals. When I say Cyber Security, it does not just limit to Pentesters / AppSec / Network / Cloud Security professionals. I see a demand for Data Privacy, Compliance and Legal folks who can understand, interpret complex regulations from the Regulators like RBI, SEBI & IRDA and help implement them in a creative, scalable and rapid way. I am currently working for an emerging Fintech company and a good chunk of my time is spent with the Legal team apart from the engineering folks in interpreting and helping fit newer technologies and controls around regulations, compliances, working on contracts, assessments, Third Party Risk management and etc

As a cyber security professional, I wouldn’t have expected to work this closely with the legal team, but no complaints and am beginning to see things from multiple perspectives! Remember that most startups live by the mantra:

“It is better to ask for forgiveness than permission”

At the end of the day, it’s all about solving problems.

If you have any questions, comments, feel free to post them here and I will try to answer them.

#fintech #cybersecurity #fintechsecurity #RBI #SEBI #IRDA #PCIDSS